Life is for living... not worrying

Insurance

No one knows what’s around the corner. It’s a fact of life

that every day, Australians just like you are faced with lifechanging

tragedy. An unexpected death, a serious health

crisis or a debilitating accident don’t just come with a high

emotional cost, they can have a serious and far-reaching

impact on finances, too. We can’t prevent life’s unexpected

events, but we can be better prepared.

We all expect that life will have its ups and downs, but what would happen if that little bump in the road became something far more worrying? What would happen if you or your partner could no longer work? How would your bills be paid? And what if you weren’t there at all? While it’s something we’d prefer not to think about, with a little forward planning and a practical insurance plan, you can get on with life knowing that you and your family would be financially covered if the worst was to happen.

Insurance is never going to compensate for the loss of a loved one, a tragic accident or serious illness, but it can help ease the financial burden and provide you with choices for the future.

Counting the cost of care

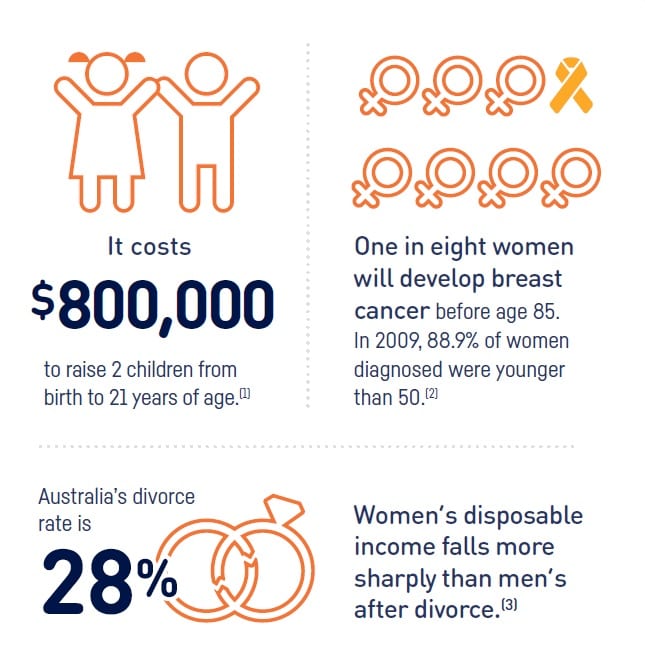

It’s a sad fact that every year around 4400 Australian parents with dependant children die. Many more are sidelined due to illness or injury.

(6)What would happen if you or your partner were no longer there to care and provide for your family?

Stay at home parents spend an average of 6.6 hours each day looking after children along with shopping and housework.

(4) If a nominal value of just $20 per hour was placed on this work, employing a housekeeper or carer to do the same work would cost around $924 for a seven day week or $48,000 over a year.

This simple calculation demonstrates the importance of insurance for both working parents and stay at home carers. Only 50% of all Australian mothers have life insurance policies, more often than not through super. And only one in five mums who work full time has enough insurance to cover their income for three years or more. This falls well short of the recommended guidelines.(5)

Unless you’re independently wealthy, adequately insuring both parents is the only way to safeguard your family’s financial wellbeing.

A family losing a mother may find that the cost of home help and child care for very young children is in excess of $75,000 per year.

– RICHARD GILBERT CEO Investment and Financial Services Association

Insurance needs checklist

If any answer is yes, you should talk to Infocus about your insurance

options for managing personal risk.

1 Do you have a partner or children who depend on you?

2 Would your dependants have enough money to live on if you weren’t

around or were unable to care for them?

3 Would your financial position be compromised if you were faced

with serious illness or injury?

4 Could you afford the costs if you or your partner were faced with

medical expenses, nursing care or extended time off work to recover?

5 Do you have a mortgage?

6 Do you have credit card or other personal debts?

Some sobering facts of life

What If?

An insurance case study

Like most people, Jenny 37 and James 41 thought that “it will never happen to us.” With Jenny earning over $100,000 a year in a career she loved, they decided that James would become a stay-at-home dad to look after their two young children with plans to return to work when the children started school.

Reliant on Jenny’s income, their Financial Adviser suggested that both Jenny and James would be wise to have life insurance. Cover for the value of their mortgage plus a lump sum to provide an income stream for child care and future school fees would provide peace of mind if something were to happen to either of them. Following this advice, they combined term life insurance with some trauma cover.

A year later, James was diagnosed with a terminal cancer. When his condition worsened, they were able to use their trauma insurance benefits to pay off their mortgage. As James was struggling with caring for the children, Jenny was able to reduce her work days so she could be there for her family.

James died eight months later. His term life insurance policy meant Jenny was in the position to take four months unpaid leave to be with her children when they needed her most. The policy pay out enabled trust accounts to be established for the children’s future as Jenny slowly put their lives back together and planned her eventual return to work.

Insurance for your peace of mind

Term life insurance

This type of insurance pays a lump sum in the event of your death or

diagnosis of a terminal illness. At such a difficult time, the last thing

your family need to worry about is money. The benefits could be used

to pay off the mortgage and other debts, provide for your children’s

current and future education needs, and simply act as a safeguard for

your family’s financial wellbeing. Life insurance is available from age 10

to 69 and it may even cover you up to age 99. You don’t need to be in

the paid work force to apply for term life insurance.

Trauma insurance

On the diagnosis or occurrence of one of a list of specified injuries

and illnesses such as heart attack, cancer or stroke, this type of

cover provides a lump sum payment. Trauma insurance provides you

with valuable choice and flexibility. If you need to make temporary or

permanent changes to your life style such as reducing work hours,

adapting your home to cope with a disability, or simply spending more

time with your family or doing the things you love, you can. You don’t

need to be in the paid work force to apply for trauma insurance.

Income protection insurance

If you are unable to work because of an illness or injury, this type of

insurance provides you with a regular payment to replace lost income.

Eligibility requirements can vary between different insurance providers.

You will be required to meet the working requirements of their policy,

which may range from 20 to 25 hours of work per week or take into

account how many weeks you actually work in a given year.

The premiums for income protection insurance are tax deductible.

Source

1 https://www.abc.net.au/news/2013-05-23/kids-eat-into-family-budget-like-never-before/4708076

before/4708076

2 canceraustralia.gov.au/affected-cancer

3 canberra.edu.au/centres/natsem/publications

4 abs.gov.au/AUSSTATS/abs

5 “Australian Mothers - Undervalued and underinsured”, IFSA Media

Release, 5/10/2005.

6 “Fast Facts: A nation exposed”, IFSA Media Release, 5/8/2005.

To learn more about insurance and

how you can protect you and your family,

talk to Brendon today

Phone now

2024 © Greythorn Financial Services

Greythorn Financial Services Pty Ltd ABN 48 477 113 239 is a Corporate Authorised Representative of Infocus Securities Australia Pty Ltd ABN 47 097 797 049 AFSL and Australian Credit Licence No. 236523

Infocus Securities Australia Pty Ltd ABN 47 097 797 049 AFSL and Australian Credit License No. 236523. This information is of a general nature only and neither represents nor is intended to be specific advice on any particular matter. Infocus Securities Australia Pty Ltd strongly suggests that no person should act specifically on the basis of the information contained herein but should seek appropriate professional advice based upon their own personal circumstances. Although we consider the sources for this material reliable, no warranty is given and no liability is accepted for any statement or opinion or for any error or omission.

Information published on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained in this document is General Advice and does not take into account any person & particular investment objectives, financial situation and particular needs. Before making an investment decision based on this advice you should consider, with or without the assistance of a qualified adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. Past performance of financial products is no assurance of future performance.