The importance of budgeting

Budgeting

One of the most important steps you can take on the road to financial security is to prepare a sustainable budget beforehand. This will help give you the foundation you need to build an effective financial plan that is realistic, achievable and tailored to your own individual circumstances.

Talk to us about effective budgeting.

Budgets are a vital aspect of financial planning because they identify

the capacity you have for saving and investing. By taking a closer look

at your income and outgoings, it’s easier to identify surplus cashflow

that could be used to reduce debt, save for the future and bring your

financial goals one step closer.

To get started, first download a budget planner at infocus.com.au or

request one from your Financial Adviser. Alternatively, you can search

online, visit your bank or find a personal finance app that includes one.

Once you’ve got your budget planner, you should block out some time for the task, and be prepared to look honestly at your spending patterns. Budgeting needn’t be complex, and revolves around two straightforward questions:

What’s coming in?

Firstly, list all forms of income. As well as salaries, consider other forms of income such as interest on bank accounts, share dividends, child support, Centrelink payments or rental income from investment properties.

What’s going out?

Start with all the regular outgoings such as bills, home loan payments, travel expenses and groceries. Then consider any annual or occasional expenses like holidays, birthday gifts, restaurant meals or vehicle servicing.

If you have more money coming in than going out, the surplus can be used for investment or savings purposes. That’s a great position to be in, and the next step is to talk to an Infocus Financial Adviser who will help you make the most of it.

If you are only just covering your outgoings, or have more money going out than coming in, it’s time to look at ways to boost your income or cut back on your spending.

Putting your savings to good use

Once you’ve isolated some savings, it’s time to put this surplus cash to work for your financial future. Here are some tips for successful saving:

• Find a savings account that offers a high rate of interest on your money.

• Ensure that interest is calculated daily on your account, not monthly or yearly.

• Set up an automatic direct debit from your transaction account into your savings account.

Balancing the budget

Taking on a part-time job or renting out a spare room to a student are two ways you could give your household income a boost – but you may find it is easier to save money than it is to make more.

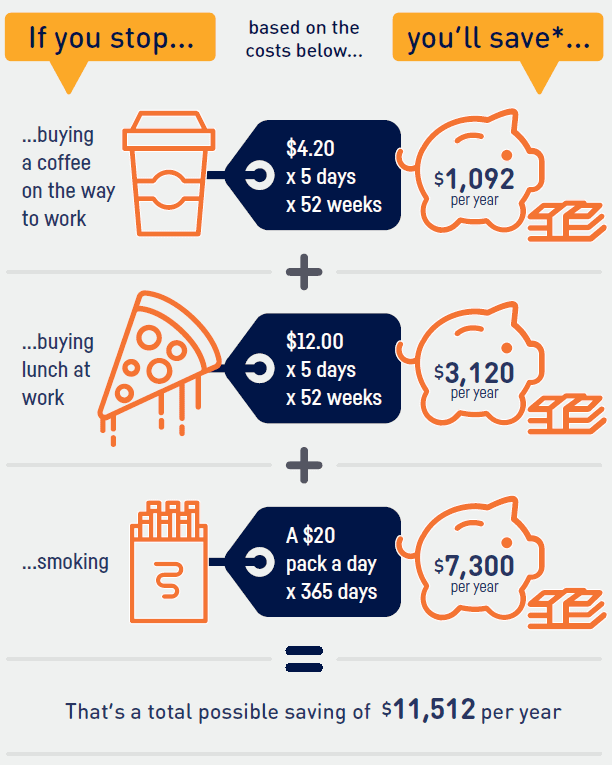

Most of us spend money on things that are ‘nice-to-have’ rather than ‘must-have’, so there are some simple savings to be made. The table below shows how small changes can make a big difference to our

disposable income over time.

A strategy for success

In essence, good budgeting comes down to common sense and discipline. So it’s important to be realistic about your spending, and not set yourself targets that you can’t reach. For instance, you are better off switching your weekly cinema trip to a day when entry is cheaper, than it is to decide not to go at all.

Similarly, planning to live on baked beans is not practical, no matter how much money you might save. Above all, remember that budgeting is all about bringing the best out in your situation. Small sacrifices you make now could lead to a brighter financial future down the track.

Searching out the savings

There are plenty of other ways to cut your outgoings. Keep the following tips in mind and you’ll soon see your weekly or monthly outgoings drop.

• Look around for a better home loan rate or have a mortgage broker search for you.

• Investigate whether solar power could save you money on hot water or electricity.

• Shop around when your insurance is up for renewal and ask about multi-policy discounts.

• Change to energy-efficient globes that last longer and are better for the environment.

• Try the supermarket-own grocery brands that provide great savings every week.

• Wrap up warm in winter with a jumper, rather than turning the heating up high.

• Dry clothes on a line not in a machine and look for more efficient models for white goods.

• Find out if you are paying bank fees and look around for fee-free options.

Keeping your cards under control

It’s also a good idea to look at the way you are using loans and credit cards, and ask

yourself if you’re paying more in interest than you need to. Here are some tips for reducing exposure to interest:

• Pay off credit cards each month (if you can) or as much as you can afford.

• Consolidate multiple loans into a single loan with a lower interest rate.

• Switch credit card debt to an interest-free balance transfer deal.

• Switch your spending to a debit card and only spend what you can afford.

• Don’t buy things on credit, if you can’t afford to buy them in cash.

Investing for the future

With the money you’ve saved through careful budgeting, you could begin an investment plan that helps deliver a more prosperous financial future.

Your Financial Adviser can tailor this investment plan for you, based on your needs, lifestyle goals and risk profile. They can also help reduce your tax liability, potentially leaving you with more money to invest.

To learn how you could turn

your savings plan into a hardworking

investment plan, talk to Brendon today

Phone now

2024 © Greythorn Financial Services

Greythorn Financial Services Pty Ltd ABN 48 477 113 239 is a Corporate Authorised Representative of Infocus Securities Australia Pty Ltd ABN 47 097 797 049 AFSL and Australian Credit Licence No. 236523

Infocus Securities Australia Pty Ltd ABN 47 097 797 049 AFSL and Australian Credit License No. 236523. This information is of a general nature only and neither represents nor is intended to be specific advice on any particular matter. Infocus Securities Australia Pty Ltd strongly suggests that no person should act specifically on the basis of the information contained herein but should seek appropriate professional advice based upon their own personal circumstances. Although we consider the sources for this material reliable, no warranty is given and no liability is accepted for any statement or opinion or for any error or omission.

Information published on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained in this document is General Advice and does not take into account any person & particular investment objectives, financial situation and particular needs. Before making an investment decision based on this advice you should consider, with or without the assistance of a qualified adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. Past performance of financial products is no assurance of future performance.